Is the middle class of old going, going, gone? Yes and the sooner we take our heads out of the sand of denial, the sooner we can strategize and create positive job solutions.

Here are economic facts of the last 40 years:

In previous recessions (2001, 1990-1991, 1981-1982, 1973-1975) mid pay jobs rebounded each time, but the net effect was still lost midpay jobs with each recovery.

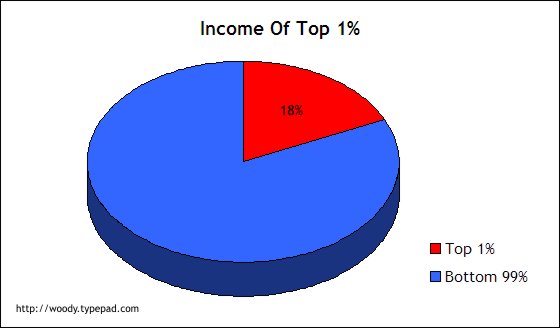

In the recovery of 2001 there was a 5% net loss of midpay jobs, in 1990-91 a 20% netloss of midpay jobs, in 1981 32% net loss. In other words with each recession the recovery of midpay jobs has declined. The net effect is that the middle class has lost ground with each recession and recovery period. “Half of the 7.5 million jobs lost during the recession were in industries that pay middle-class wages, ranging form $38,000 to $68,000. But only 2% of the 3.5 million jobs gained since the recession ended July 2009 are in midpay industries.* Mid-wage jobs were 60% of recession losses but only 22% of recovery growth.

What about the poor? How do two working adults make enough money for rent, food and basic necessities on a $7.25 an hour minimum wage? They don’t. In California, the miniminum wage is $8.50 an hour. If the minimum wage was pegged to inflation over the past 40 years, the federal standard would be $10.58 an hour.* Still not much to build a better life on.

Who or what is to blame? It's more complex than this answer, but technology is the major culprit, though of course the housing market and banking excesses share the blame. Though we love our technology, it is the main problem in terms of recapturing lost mid wage jobs because robots, software and newer and better apps do jobs faster, cheaper and more productively than humans can. Companies understandably go for increased productivity and earnings and cheap, effecient labor.

What's the solution? First of all, letting go of the dream that things will go back to the way they were. Forget it. Let's move on. Then, we need our best, most creative economists, along with folks from the middle class and poor to brain storm short and long term solutions to job creation because, believe me, we are all in this economic soup together. If the middle class and poor continue to lose ground that affects all of our standard of living. We can create job solutions. We must start now and we can't leave that to Washington alone. (*“The Great Reset, Recession, technology kill middle-class jobs,” Modesto Bee January 27, 2013, ** Michelle Singletary, Mod Bee 1-27-2013)